Summary

UPS is rated SELL. They are an important component of the American economy, known for their brown trucks. Their projected growth rate and dividend projects a 9% return on investment, which doesn’t meet our investment goal of 15%. The projections for growth rate takes into account the prominent success UPS has had at growing their business while also noting the challenges from competition and macroeconomic conditions.

Understanding UPS as a Business

UPS is the world’s largest package delivery company. UPS offers a wide range of transportation, logistics, and supply chain management solutions. UPS’ revenue streams include domestic package, international package delivery, supply chain & freight.

Domestic package delivery is by far their biggest revenue stream. UPS operates a vast network of ground and air transportation services, catering to both business and residential customers. The company offers a variety of options for shipping, including next-day delivery, two-day delivery, and ground services. Everyone recognizes their brown trucks driving around their neighborhood and their brown boxes on their porches. This service is one of the largest components of the ecommerce economy. Someone buys something online and it gets shipped via UPS. This sector is reliant and representative to the American macro economy.

UPS also has a significant presence in the international shipping and delivery market. It provides cross-border logistics, air and ocean freight services, customs brokerage, and international express delivery to businesses and consumers globally. This segment involves delivering packages and freight across borders and managing global supply chain solutions.

UPS also generates revenue through its supply chain and freight segment. This division includes freight forwarding, truckload brokerage, distribution, and contract logistics services. It caters to businesses seeking comprehensive supply chain solutions, warehousing, and transportation management services.

UPS does have a significant moat with their extensive physical infrastructure. This includes their trucks, planes, warehouses, and fulfillment centers. Despite the large moat that UPS has built there are still a few competitors in the space. The most prominent competitors being FedEx and Amazon.

Valuation Metrics

The finviz stock screener is a great tool to see performance metrics that are important to assess a company’s valuation.

With a market capitalization of $129 billion, UPS is presently evaluated at a Price-to-Earnings (P/E) ratio of 15, a figure aligned with its anticipated future P/E. Considering the current earnings of $9.89 per share and a robust dividend yield of 4.26%, the company’s valuation appears reasonably balanced. Projections suggest a slight decline of 4.75% in earnings over the upcoming five years, which could be influenced by specific short-term factors, like the substantial downturn experienced in 2023, potentially requiring a recovery period before returning to positive growth trajectories. Despite this anticipated decline, UPS’s solid fundamentals, along with its dividend yield and consistent earnings, remain attractive components for investors seeking a stable investment option in the logistics sector.

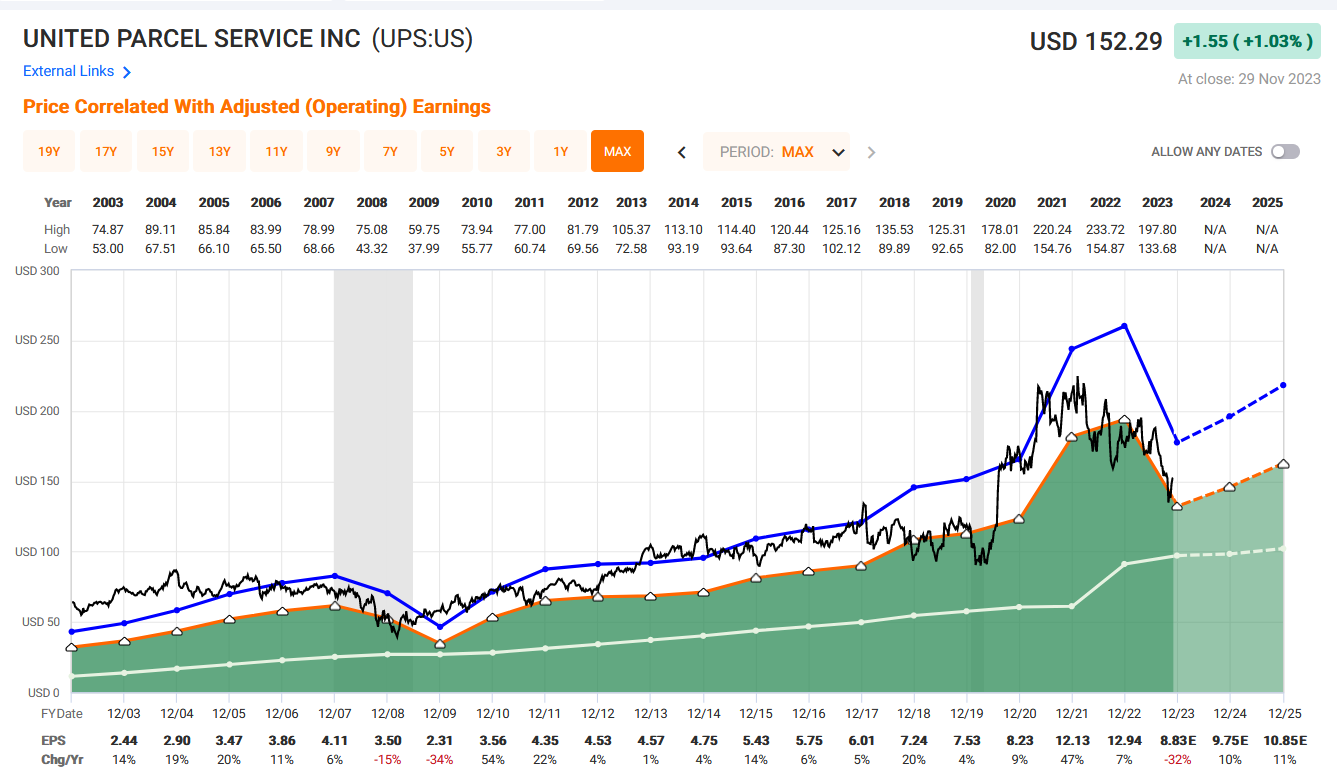

FAST Graphs

The FAST Graphs software is a powerful tool used to analyze the earnings of a company compared to the share price. The black line is share price and the orange line is earnings multiplied by 15.

Looking at FAST Graphs we can see the share price is near the fair value line however the fair value line is in a current down trend. We can see that the projections for their earnings turn around past 2023.

Bull Thesis

UPS remains a pivotal player in the U.S. economy, wielding a formidable position fortified by a robust competitive advantage. Despite a challenging 2023, which has been factored into the current valuation, UPS exhibits promising prospects beyond this period. This temporary setback offers a compelling opportunity to invest in a stalwart company at a favorable valuation. Amidst the surge in e-commerce activities, UPS stands primed to leverage this burgeoning market trend, fostering potential for substantial earnings growth in the forthcoming years. Additionally, UPS’s ventures into international markets underscore its strategic expansion plans. Leveraging its extensive institutional knowledge and logistical prowess, UPS is poised to replicate its successful domestic delivery infrastructure on a global scale. This strategic move holds the potential to bolster earnings significantly while unlocking new avenues for shareholder value creation. As UPS navigates through these growth trajectories, it positions itself as a promising investment prospect for those seeking exposure to a resilient company ready to capitalize on evolving market dynamics and drive future earnings growth.

Bear Thesis

UPS experienced a notable earnings decline in 2023, attributed to various factors, including a challenging macroeconomic environment and intensified competition within the logistics sector. In contrast, FedEx exhibited a relatively better performance, maintaining earnings levels more effectively than UPS during the same period. Furthermore, the formidable rise of Amazon poses a substantial threat. Amazon’s relentless expansion of its retail dominance and continuous enhancements in delivery infrastructure could potentially encroach upon UPS’ market share. As Amazon fortifies its logistics capabilities, there’s a looming possibility that it might further challenge UPS’ foothold in the industry. Considering these trends, the growth trajectory of UPS seems constrained. The lack of robust earnings growth raises concerns about the company’s ability to generate the desired return on investment. This scenario leads to skepticism about UPS’s capacity to deliver the anticipated performance levels, creating doubts among potential investors seeking higher growth opportunities.

Rating

UPS is rated SELL. While UPS is a stalwart in the American economy and boasts a reliable dividend, it falls short of meeting our investment goals. The market’s anticipation of a 5% earnings growth over the next few years already factors in prevailing challenges, including heightened competition from FedEx and Amazon, alongside broader macroeconomic uncertainties. Although the dividend offers a degree of stability, it doesn’t compensate adequately for the anticipated sluggishness in earnings growth. Despite being a stalwart in the industry, UPS doesn’t align with our current investment criteria, as we seek opportunities that promise more robust returns and growth potential.