Summary

Altira is rated a BUY. Altria has a great opportunity for its share price to return to a normal trading multiple of between 14 and 15. The return to the mean won’t happen because of a fall in earnings because earnings are projected to continue to grow at 4% for the long term. Analysts have a great track record of predicting earnings due to its predictable customer base. The margin of safety with its 9% dividend means that if the multiple doesn’t return to the mean you will still see a return on investment that is close to the goal of your portfolio.

Understanding Altria as a Business

Altria’s core business is the manufacturing and sale of tobacco products, primarily cigarettes and smokeless tobacco. It owns some of the most well-known tobacco brands in the United States, including Marlboro, Copenhagen, and Skoal. These brands are distributed nationwide through various channels, including retail stores and wholesalers.

Altria is adapting to changing consumer preferences and evolving regulations by investing in and developing reduced-risk tobacco and nicotine products. This includes electronic cigarettes and heated tobacco products. Altria produces and markets smokeless tobacco products such as snuff and chewing tobacco under the Copenhagen and Skoal brands. Smokeless tobacco is seen as a potentially less harmful alternative to smoking.

Altria has an amazing moat to protect them from competition. The brand loyalty among smokers is sky high and people won’t switch to the competition. Smoking itself has a big moat that it is incredibly addicting and the people that are addicted will keep buying cigarettes.

The risk to the Altria business is that less people are smoking. The public opinion on smoking is very negative and that is a shrinking potential customer base. The health concerns of smoking are real and people ought not to be smoking.

Valuation Metrics

The finviz stock screener is a great tool to see performance metrics that are important to assess a company’s valuation.

The market cap of Altria is $79 billion. The P/E is approximately 12 which is below its historical average of 15. The impressive performance with this company is its nearly 9% dividend. That is over half way to the goal of 15% return on our investment. The earnings are expected to grow at 4% per year. This expectation can be taken at face value because the tobacco industry is accurately predicted by analysts year over year.

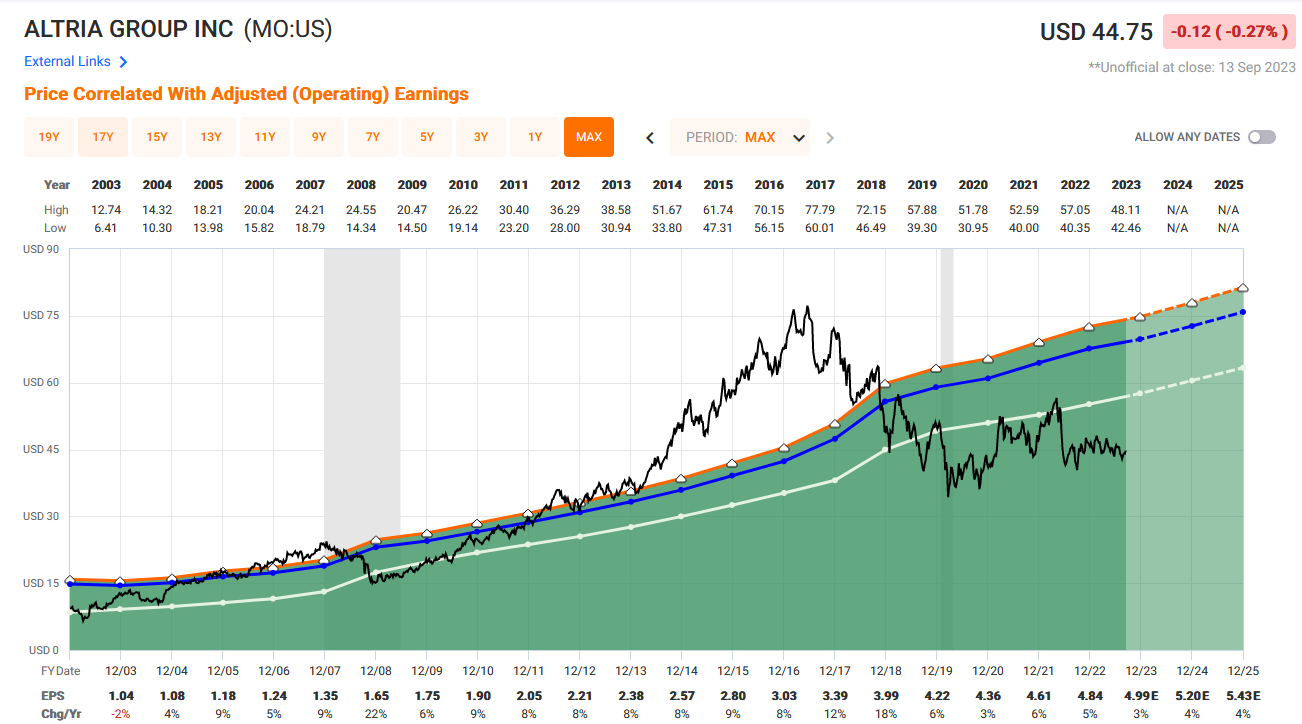

FAST Graphs Analysis

The FAST Graphs software is a powerful tool used to analyze the earnings of a company compared to the share price. The black line is share price and the orange line is earnings multiplied by 15.

As you can see the share price is far below the earnings line. This would represent to us that Altria is undervalued compared to its earnings; the share price is due to catch up with its earnings. The growth rate isn’t very high however the dividend is large and the earnings are high compared to the share price.

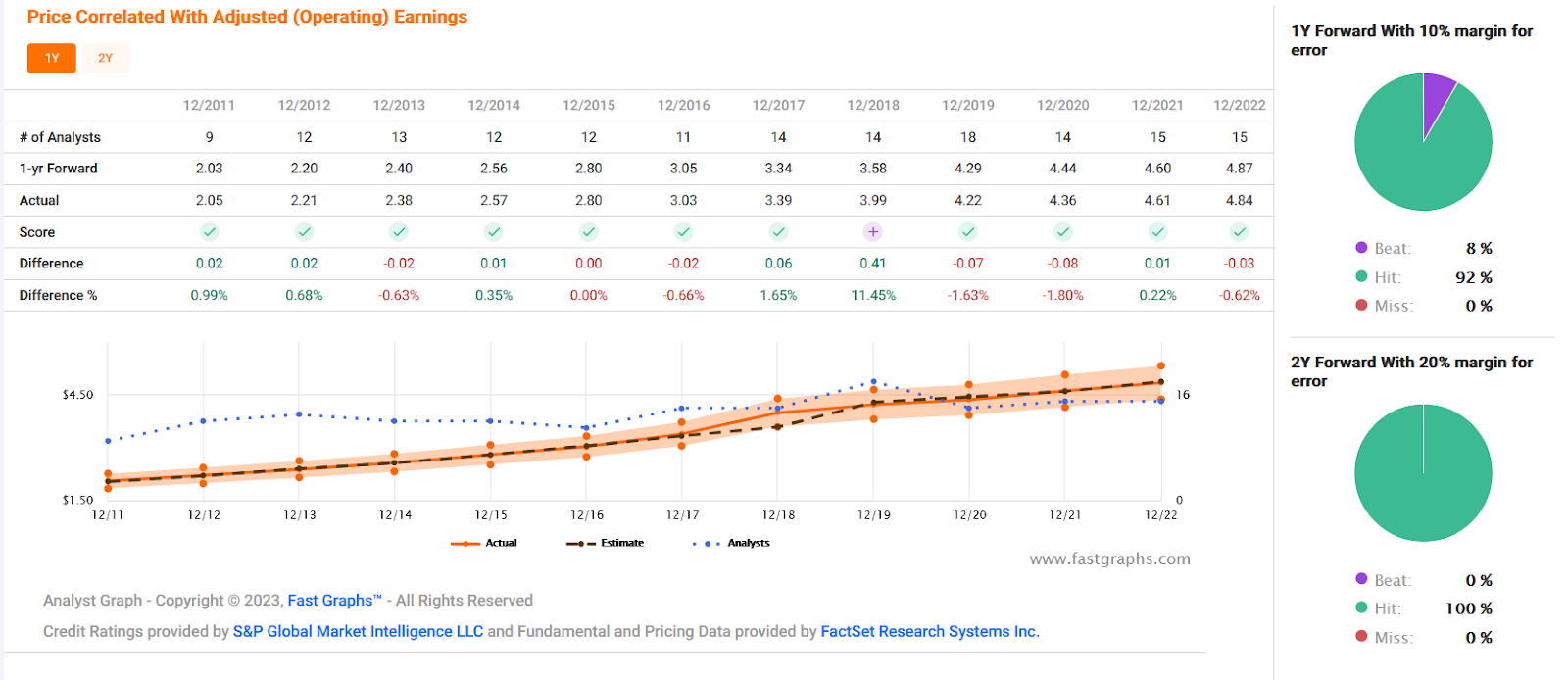

Another tool that FAST Graphs offers is the analyst scorecard here we can see how accurate the analysts have been at predicting Altria’s earnings.

Here we can see that analysts don’t miss on predicting Altria’s earnings. This comes from a predictable customer base along with a good understanding of the company long term. This allows us to use forecasts to our advantage when thinking about future performance.

Bull Thesis

Altria has a base of customers that is inelastic. In a market down trend their customers will still be buying their products. As cigarette sales decrease due to public perception of smoking, Altria will replace cigarette sales with other products such as the vaping products and smokeless products. Analysts have a great track record of being able to predict the earnings at a 92% hit rate with a 10% margin of error. The analysts are predicting that the earnings are to stay consistently growing at a marginal rate of 4%. A 4% earnings increase and a 9% dividend yield at the current multiple would be 13% gain. This is close to the goal of 15% return for the portfolio. The investment thesis is based on the return to mean of the trading multiple of between 14 and 15.This would be a return of 100% over the next few years. This combined with the dividend yield of 9% of our current investment would be in line with providing us our investment goal of 15% gain.

Bear Thesis

This company’s main product for its history is cigarettes. Cigarettes are on their way out because people realize the health effects and the public perception is incredibly low. The low multiple currently applied to the company is because of the low growth of the company. Eventually the cigarettes will fall away and earnings will decline and the dividend will decrease.

There won’t be a return to the mean of the multiple for the share price because the company is fairly valued for the low growth and eventual demise of tobacco products. The return with earnings growth and dividend won’t meet the investment goal of the portfolio.

Rating

Basil Leaf Capital rates Altria a BUY. The return to the mean of the earnings multiple offers a great opportunity to return greater than the portfolio goal of 15%. The analysts have a great track record of predicting earnings and the analysts predict steady earnings growth over the next few years. This would warrant a return to the mean of the trading multiple of between 14 and 15. Even if the return to the mean isn’t all the way back to 15 it still offers a good opportunity for return on investment. Along the same lines as margin of safety this stock offers a margin of safety if it never returns to the mean and trades at a 9-10 multiple as a new normal. A 4% growth in earnings and 9% dividend yield gives a total of 13% return without taking into account dividend growth. This is a great margin of safety with an opportunity for major returns.