Summary

3M is rated a BUY. 3M manufactures adhesives and safety products in a multitude of industries. 3M has great upside with a return to a normal multiple while offering a margin of safety with earnings and dividends. The company went through a large decline after a lawsuit which is why there is a great opportunity to buy this company at a decreased price. The bear case has already been priced in and is too pessimistic. 3M products are great products and the company will continue to earn profits.

Understanding 3M as a Business

3M is a multinational conglomerate that is known for its diverse portfolio of products. 3M breaks its product portfolio into 4 main segments: The safety & industrial segment, Transportation & Electronics, Healthcare, and Consumer.

The safety & industrial segment is a critical player in the safety and productivity industry and is 34% of total revenue.. It offers a broad array of products such as personal protective equipment (PPE), adhesives, abrasives, and materials for occupational health and safety. I use 3M PPE at my job such as respirators and respirator filters. Since I rely on 3M safety products for my safety in my workplace, I think these are quality products. Quality products are the bedrock of a quality investment.

The transportation & electronics segment provides materials for automotive, aerospace, and electronics manufacturing. This segment accounts for 23% of revenue. Products like adhesives and films support vehicle maintenance and repair, a necessity for the automotive industry’s continuous operation. 3M being components in all these industries provides a diversity of customers. We are not aware of all their products but they are critical in things we use everyday such as our cars.

The healthcare sector, 3M’s products include medical tapes, wound care products, sterilization equipment, and dental materials. This segment accounts for 16% of the revenue of the company. These offerings are vital for healthcare professionals and facilities worldwide. The growing global healthcare industry contributes significantly to this segment’s revenue. My wife is a nurse and uses these products in her field every day. 3M truly has put their products into every industry and maintains the same great quality.

3M as a business is great at taking similar products and technologies and applying them to different industries. They have adhesive products in all their segments. 3M’s moat includes a large market share and brand recognition in the spaces they are in. They have economies of scale for all their products and make it a challenge for new businesses to enter the industry.

Valuation Metrics

The finviz stock screener is a great tool to see performance metrics that are important to assess a company’s valuation.

3M is valued at a $49.5 Billion company by market cap. The PE is not listed as a trailing 12 month metric however taking the earnings from 2023’s first 3 quarters and the projected earnings from Q4 then it is trading at a PE of 9 which is reflected in its forward PE. The projections for the earnings for the next few years is 8%. At its current price 3M is paying out a nearly 7% dividend to its shareholders.

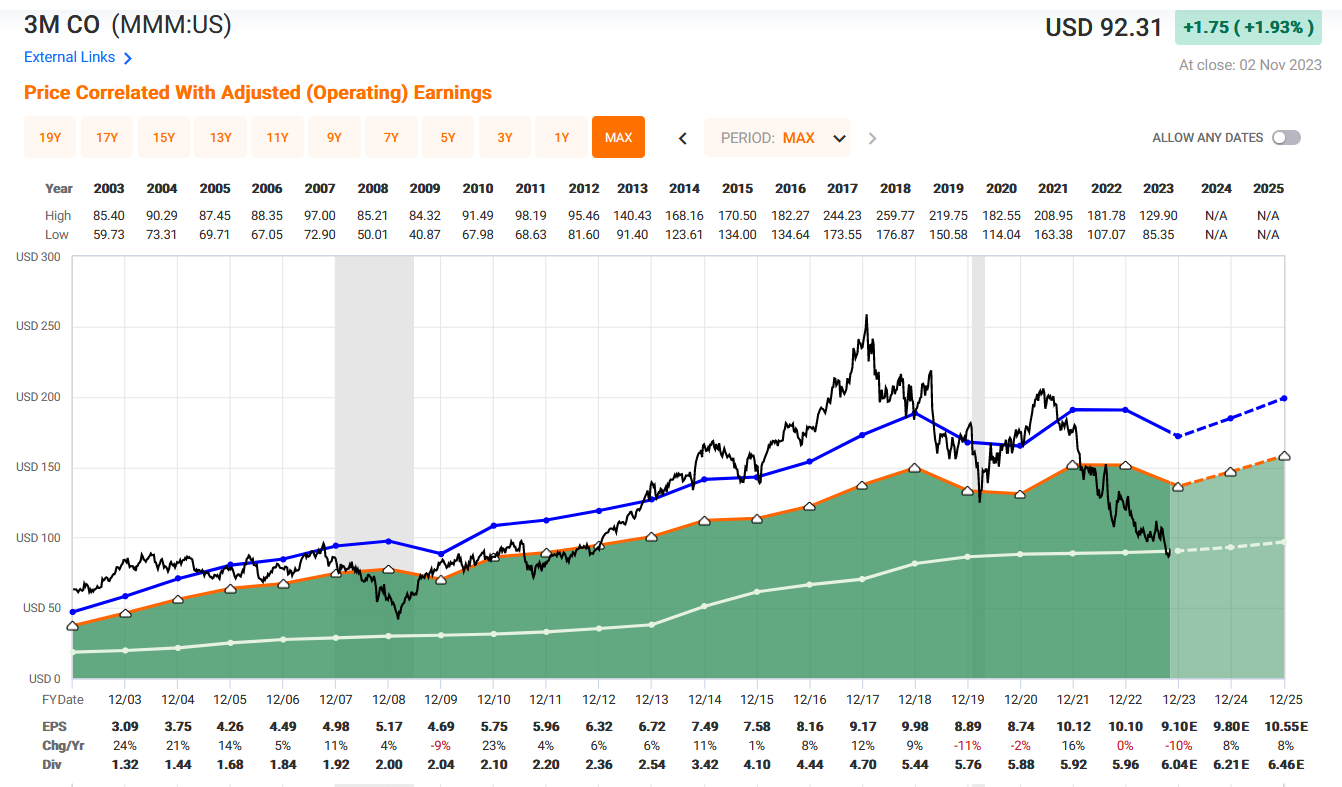

FAST Graphs Analysis

The FAST Graphs software is a powerful tool used to analyze the earnings of a company compared to the share price. The black line is share price and the orange line is earnings multiplied by 15.

The recent decline in share price has brought it below the trading multiple that it has historically traded at and what a fair value 15 multiple would be. This company is still earning money and returning shareholders value with dividends. There is still projected growth for 3M and a return to fair value.

Bull Thesis

3M is a solid company that has a diverse portfolio of products that bring in revenue and profits. Their customers love and trust their products. This brand recognition and customer loyalty is a wide moat they have in their business. Other companies will have trouble beating 3M out of their customers. 3M has a long history of delivering value to their shareholders with earnings growth and dividends. The investing goal is to return the 15% on our investment and this company can get there for us in earnings growth, dividends and multiple expansion. The company is guiding forward that earnings will grow 7% per year and earn $9.10 per share this year. It is also paying out a 6.5% dividend. 7% added to a 6.5% dividend provides us with 13.5% which isn’t quite to the 15% goal we have for ourselves. The multiple expansion will come from a return to a normal multiple or at least a fair value multiple. An expansion from a current multiple of 10 to a multiple of 15 will provide the upside we are looking for. Even if the multiple doesn’t expand then we still have a margin of safety of earnings growth and a dividend.

Bear Thesis

The current multiple is negative because in the past months 3M has been losing money in the trailing 12 months. A large part of this loss is from a lawsuit in which they lost. Alongside this lawsuit 3M is also a cyclical business that is entering a down cycle. Analysts have yet to take into account this down cycle and the reduced earnings. If 3M only provides dividends not earnings growth then we are not getting the return we are looking for in our investment portfolio. 3M is a solid company however we won’t get the return we are looking for investing in this company. We would be better off investing our money somewhere else that would return more value.

Rating

3M is rated a BUY. 3M is a great company that is at a reasonable valuation currently. We believe the company’s forward guidance and that there is room for a multiple expansion. Having first hand use of their products and trusting them for my safety is a great sign that the company will continue to have customers and make money. The earnings growth will continue and the dividends return shareholder value. The multiple expansion provides enormous upside for our investment portfolio alongside a solid return for a margin of safety. The lawsuit isn’t a bear case for the future; the price has already taken that into account. The lawsuit and seasonality provides a solid company at a great price.