Summary

AGCO is a SELL. AGCO is a cyclical business entering a down cycle with shrinking earnings. This is a potential value trap for investors and it could take years for the cycle to reverse. The only path for a return on investment is an expansion of the current multiple however we don’t want to count on value expansion on a company that’s earnings are shrinking.

Understanding AGCO as a Business

AGCO Corporation is a global leader in the design, manufacture, and distribution of agricultural solutions. The company operates in the highly cyclical and capital-intensive agriculture industry. AGCO’s revenue comes from two main sources. They are world leaders in the tractor and combine industry.

Tractors are a core product for AGCO and a significant contributor to its revenue. The company manufactures and sells a range of tractors catering to different agricultural needs, including utility tractors, row crop tractors, and high-horsepower tractors. Revenue from tractor sales is influenced by factors such as farmers’ replacement cycles, agricultural commodity prices, and global demand for agricultural products.

AGCO is a leading producer of combines, which are essential for harvesting crops. Combines are complex machines that integrate various harvesting functions, and their sales are influenced by factors similar to tractors. Farmers often invest in new combines to enhance efficiency and keep up with technological advancements.

Since these items are so expensive the demand is also heavily dependent on interest rates because farmers need to finance them to purchase them. With a high interest rate environment demand for these items could be reduced.

The agricultural product sector is incredibly cyclical. Part of management’s plan to combat this cyclical nature is to diversify into counter cycle products. The main counter cycle product is protein products. The protein products now account for ⅓ of the revenue. This helps balance the cyclical nature of the business.

Valuation Metrics

The finviz stock screener is a great tool to see performance metrics that are important to assess a company’s valuation.

AGCO is valued at $8.57 Billion by market cap. The price to earnings is 7.43 and the forward PE is 7.86. What we can garner from that information is that the earnings are projected to maintain a similar level between this quarter and next quarter. The dividend yield is 6.58% because they paid a large variable dividend because their past year was a great year. The dividend won’t be consistently this big but they do pay a dividend. It is important to understand the context behind the numbers presented in these websites. Another intriguing metric is that the price to sales ratio is only 0.59. This means you only have to pay $0.59 for every $1.00 of revenue AGCO earns. Earnings are projected to go down next year but positive growth over the next 5 years. This suggests we are going into the down cycle.

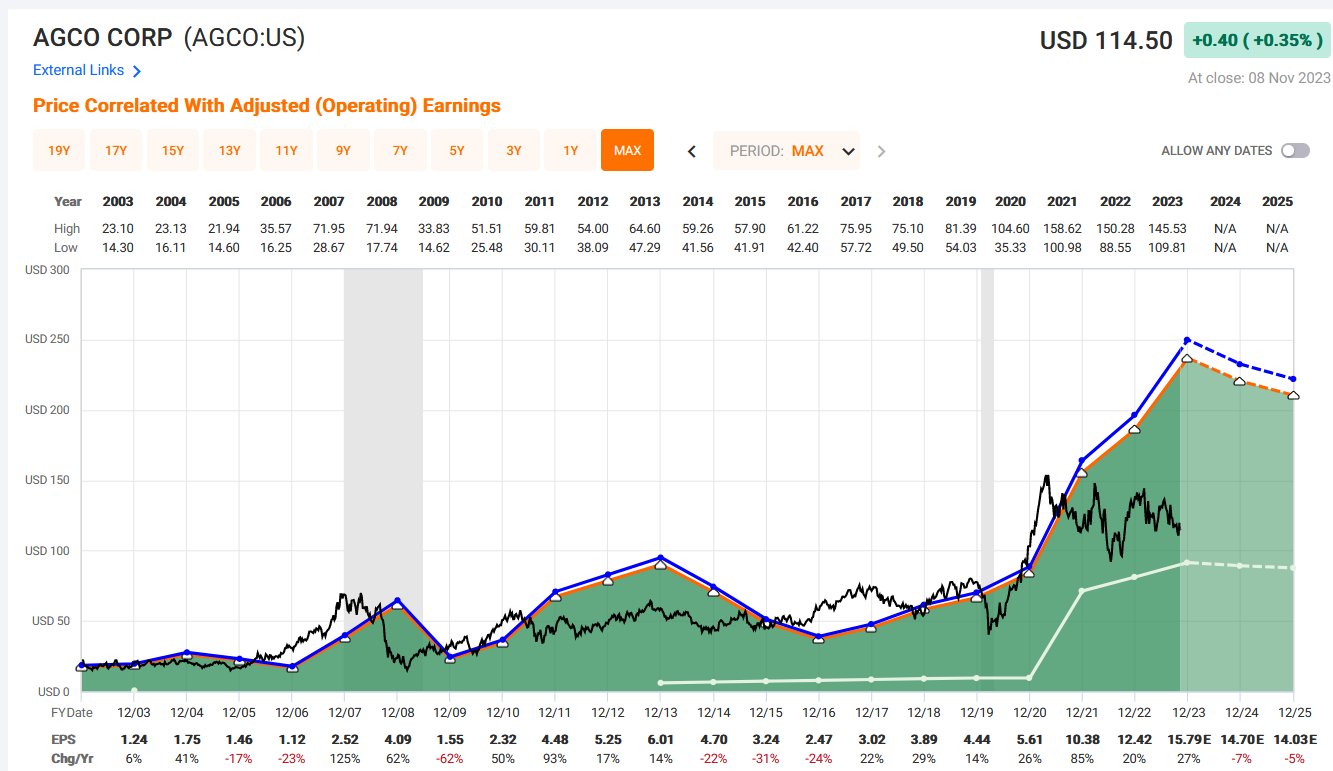

FAST Graphs Analysis

The FAST Graphs software is a powerful tool used to analyze the earnings of a company compared to the share price. The black line is share price and the orange line is earnings multiplied by 15.

AGCO price has been on the decline since 2020 while earnings were going up. The cyclical nature of the business can also be seen across the history of the earnings. The earnings are projected to decrease over the next couple years due to a down cycle. Even with an earnings decline the share price is still below what would be a fair value at those reduced earnings.

Bull Thesis

AGCO has dramatically increased its earnings since 2016 and the share price really never caught up. AGCO makes quality products and is diversifying its strategy to reduce its cyclical nature. In the long term the grain storage industry and protein product industry are projected to grow from a macro sense. AGCO is well positioned to take advantage of this macro trend and not have such a poor down cycle. The reason that the multiple hasn’t followed the increased earnings is because analysts believe the down cycle is around the corner and the earnings will come back down. Historically the company has down cycles but they have higher lows to go along with the higher highs and the share price is too pessimistic on the future earnings. We’ve seen in two other previous cycles that the share price bottoms soon after the peak of earnings. Based on that trend we could be near the bottom of the share price for this cycle and the share price recovers through a multiple expansion. If the analysts are correct in the earnings reduction and the price returns to a normal multiple of those reduced earnings we could see a return on investment of 36%. Even if we only got half of the return to the normal multiple we are still looking at a return of 18% per year which is greater than our goal of 15% return.

Bear Thesis

AGCO is an incredibly cyclical business and we are entering a down cycle. The earnings are projected to shrink in the coming years. The multiple is this low because the earnings will be going down. The return on an investment tracks earnings and earnings being reduced means that investing in the company isn’t a profitable endeavor. The dividend is dependent on revenue, free cash flow, and earnings. The earnings are going to be reduced and so will the dividend. The only path currently to beat our return rate of 15% is for multiple expansion in a stock that is shrinking earnings.

Rating

AGCO is rated a SELL. AGCO is in a down cycle currently and will have shrinking earnings for the next few years. This is not the correct time to be buying a company when its earnings are shrinking. The company is a solid company however the timing currently is not the right time. AGCO is a solid company however we could achieve better returns on investments in companies whose earnings are growing currently. We agree with the bull case that share prices could be near the bottom, however it could take years for the cycle to reverse and we could invest in something that returns more during the time it takes for AGCO to recover.