Summary

Alibaba is rated a BUY. Alibaba has Robust fundamentals and offers an earnings growth rate of 12% year over year and price to earnings expansion from 10 to 15. This would offer a return on investment of a potential 40% year over year return. There are a few concerns regarding the fundamentals such as competition joining the market and relying almost entirely on the domestic Chinese market. These concerns are priced into the 12% projected growth rate and we can trust the management to continue strong execution.

Understanding Alibaba as a Business

Alibaba is a large conglomerate composed of many different brands and websites to generate revenue. Alibaba is a large player in the ecommerce space and most noticeably how a lot of drop shipping companies supply their customers with products. Being such a large conglomerate they have multiple different revenue streams.

Alibaba’s largest revenue stream is Core Commerce. It includes the platforms such as Taobao, Tmall, and Alibaba.com, which facilitate business-to-consumer (B2C) and consumer-to-consumer (C2C) online retail. Revenues are generated through commissions, advertising, subscription fees, and other value-added services for sellers. Alibaba will supply the products from the manufacturers and then businesses can market and advertise these products as their own. These are typical cheap chinese products that take a long time to ship from China to America.

Cloud Computing is Alibaba’s second biggest revenue stream, known as Alibaba Cloud Computing, provides cloud infrastructure, data management, and artificial intelligence services to businesses and government entities. It generates revenue through subscription fees, usage-based charges, and other cloud-related services.

Alibaba owns various entertainment platforms, including Youku (a video streaming service) and UCWeb (a mobile internet software and services provider). Revenue is derived from advertising, subscriptions, content licensing, and other digital entertainment services.

Alibaba also invests in newer initiatives in areas like logistics, local services, and new retail. Revenue comes from various sources, including logistics services fees, local consumer services, and other innovative projects.

Valuation Metrics

The finviz stock screener is a great tool to see performance metrics that are important to assess a company’s valuation.

Alibaba is valued at $180 Billion by market cap. It currently trades at 10.3 Price to Earnings ratio. Its forward PE is 7.82 based on its projected growth rate. Over the next 5 years it is expected that Alibaba will grow earnings at a rate of approximately 12%. Alibaba has recently also declared a 1% dividend. At its current valuation the earnings seem to be at a fair to undervalued valuation.

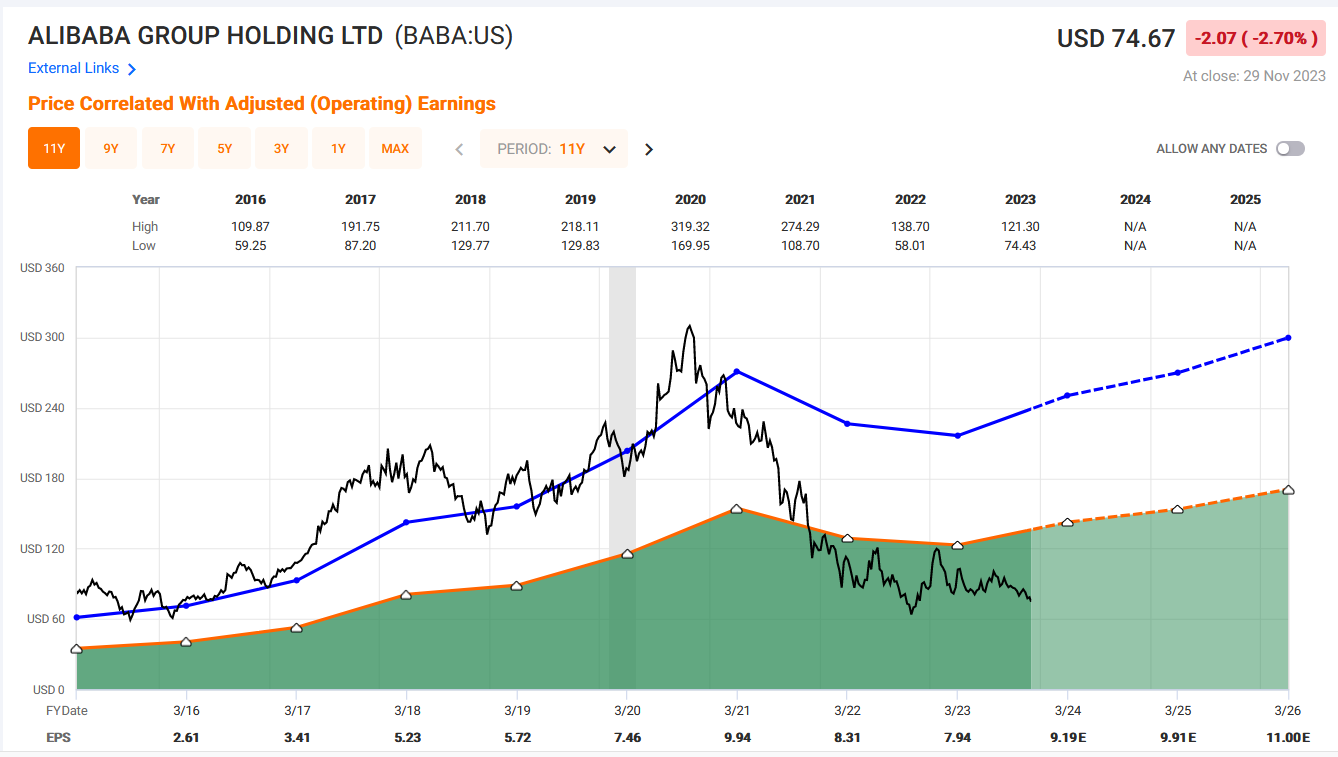

FAST Graphs Analysis

The FAST Graphs software is a powerful tool used to analyze the earnings of a company compared to the share price. The black line is share price and the orange line is earnings multiplied by 15.

Alibaba historically traded well above the 15 PE range and even above the blue line which is its average PE. Since its peak in 2020 it has been on a down trend. At its current share price looks to be undervalued based on current earnings and projected future earnings. Using FAST Graphs we can see that the current and future earnings of BABA are being undervalued and there is an opportunity for significant upside when share price catches up to its earnings.

Bull Thesis

Alibaba presents a compelling opportunity to enhance our portfolio with a company poised to achieve our targeted 15% return. This growth will be underpinned by robust fundamentals, driving a steady 12% annual earnings expansion. With the present fundamentals and current valuation Alibaba could return 40% annualized return until at least 2026 if the PE returns to a reasonable valuation of 15. The return could be even greater if the PE returns to historic average of 25. Alibaba’s stronghold in the Chinese e-commerce realm is evident through its dominant presence across platforms like Taobao, Tmall, and Alibaba.com. With a diverse business portfolio spanning e-commerce, cloud computing, digital payments, logistics, and media, the company generates revenue across multiple sectors, reducing reliance on any single segment. Over the years, Alibaba has demonstrated consistent revenue growth propelled by its e-commerce activities, cloud computing, and digital entertainment divisions. Continued innovation and forays into new sectors bolster its revenue streams.Furthermore, the potential for an expanded Price to Earnings (P/E) ratio predicts well for increased upside in this investment. As Alibaba strategically expands its global footprint, the company’s international presence becomes increasingly robust. Sizeable investments in Southeast Asia, India, Europe, and the United States position Alibaba for substantial growth beyond its domestic market. Moreover, its commitment to research and development is paramount. By investing in cutting-edge technologies like artificial intelligence, big data, and IoT, Alibaba primes itself for future growth and sustained competitive advantage.

Bear Thesis

Alibaba, despite its prominent position in the Chinese e-commerce market, faces several potential challenges and risks that could hinder its growth trajectory. One of the key concerns involves increased regulatory scrutiny and changing government policies in China. The Chinese government has shown a tendency to introduce regulatory changes that could impact large tech companies, particularly in areas related to data privacy, antitrust measures, and market competition. Any adverse regulatory action or new restrictions imposed on Alibaba’s operations could significantly disrupt its business model, affecting revenue streams and investor confidence. An example of this is when the Chinese Government “Disappeared” Alibaba’s founder Jack Ma for a few years. There is always risk associated when a company is subjected to the whims and regulations of a tyrannical dictatorship.

Another pressing issue is the company’s overreliance on its domestic market. While Alibaba has made strides in expanding internationally, the majority of its revenue still stems from China. This concentration leaves the company vulnerable to any economic, geopolitical, or regulatory uncertainties within the region. Moreover, intensifying competition within the Chinese market poses a threat, with rivals continually vying for market share and technological advancements. JD is an example of a competitor to Alibaba and could take market share in China. Alibaba is trying to expand into international markets, specifically the US. Alibaba would have trouble competing with Amazon which is the E Commerce powerhouse in the US. The drop shipping industry is already pivoting away from using Alibaba because of poor quality in terms of products and shipping times. These competitors are bound to reduce Alibaba’s margins and therefore earnings.

The global economic landscape, including trade tensions between major economies, presents additional risks for a multinational company like Alibaba. Any disruptions in international trade or economic downturns could negatively impact consumer spending, affecting Alibaba’s revenue and growth prospects.

Rating

Alibaba is rated a BUY. Alibaba has robust fundamentals that will continue to drive its 12% earnings growth projections. The solid fundamentals have some concerns revolving around competition, and macroeconomics however those concerns are priced into the earnings projections. The earnings growth rate of 12% is solid however that alone is not enough to meet the portfolio goal of returning 15%. The upside opportunity resides in the cheap current valuation. Historically Alibaba has traded at a PE of 25 and a reasonable valuation of a company with this earnings growth would be 15. If the multiple returns to 15 from its current 10 then we can anticipate a return of around 40% year over year. This would exceed our investment goal and be a good addition to the portfolio.