Summary

Global Payments is a BUY. GPN is a payment processing company that empowers small businesses to process credit card payments. This is a quality company at a fair price. The expected growth of 14% not including the dividend, making this is a great opportunity for your portfolio to meet the return rate of 15%. Global Payment’s is a great way to get exposure into the electronic payment fintech space without too much speculation.

Understanding GPN as a Business

Global Payments is a leading payments technology company delivering innovative software and services to customers globally. Their technologies, services and team member expertise allow them to provide a broad range of solutions that enable their customers to operate their businesses more efficiently across a variety of channels around the world. Global Payments operates in 3 main segments of their business. Anytime you purchase something from a business and use your credit card, GPN could be the payment processor. They are the middle men between the credit card company and the small business.

Merchant Solutions: This segment provides businesses with a suite of payment solutions, including point-of-sale (POS) systems, card processing, e-commerce capabilities, and fraud protection services. By offering these services, GPN empowers merchants to accept a wide range of payment methods, enhancing their customer reach and efficiency.

Issuer Solutions: GPN’s Issuer Solutions segment focuses on supporting financial institutions by providing card issuing and consumer lending services. This includes credit and debit card programs and risk management services, offering banks and credit unions the tools to deliver secure and flexible financial products to their customers.

Business and Consumer Solutions: In this segment, Global Payments offers innovative solutions to meet the diverse payment needs of businesses and consumers. This includes digital banking, bill pay services, and e-commerce solutions. It bridges the gap between businesses and consumers, ensuring secure and convenient transactions.

The global payment industry is highly competitive and rapidly evolving. One of Global Payments’ significant moats is its extensive network of merchants and financial institutions. This network effect is built on trust and reliability, making it challenging for new entrants to replicate. The company’s continued investment in technology and acquisitions further solidifies its position in the market. Small businesses rely on these payment processors for their livelihood and won’t switch processors without a good reason.

However, the industry faces challenges, including rapidly changing consumer preferences, increased regulation, and evolving security threats. Staying ahead in the fast-paced world of digital payments requires ongoing innovation and adaptability.

Valuation Metrics

The finviz stock screener is a great tool to see performance metrics that are important to assess a company’s valuation.

Global Payment Networks is valued at $30 Billion by market cap. The price to earnings ratio based on the trailing earnings is 38. The future P/E is projected to be 10. The growth rate is expected to be 14% for the next 5 years.

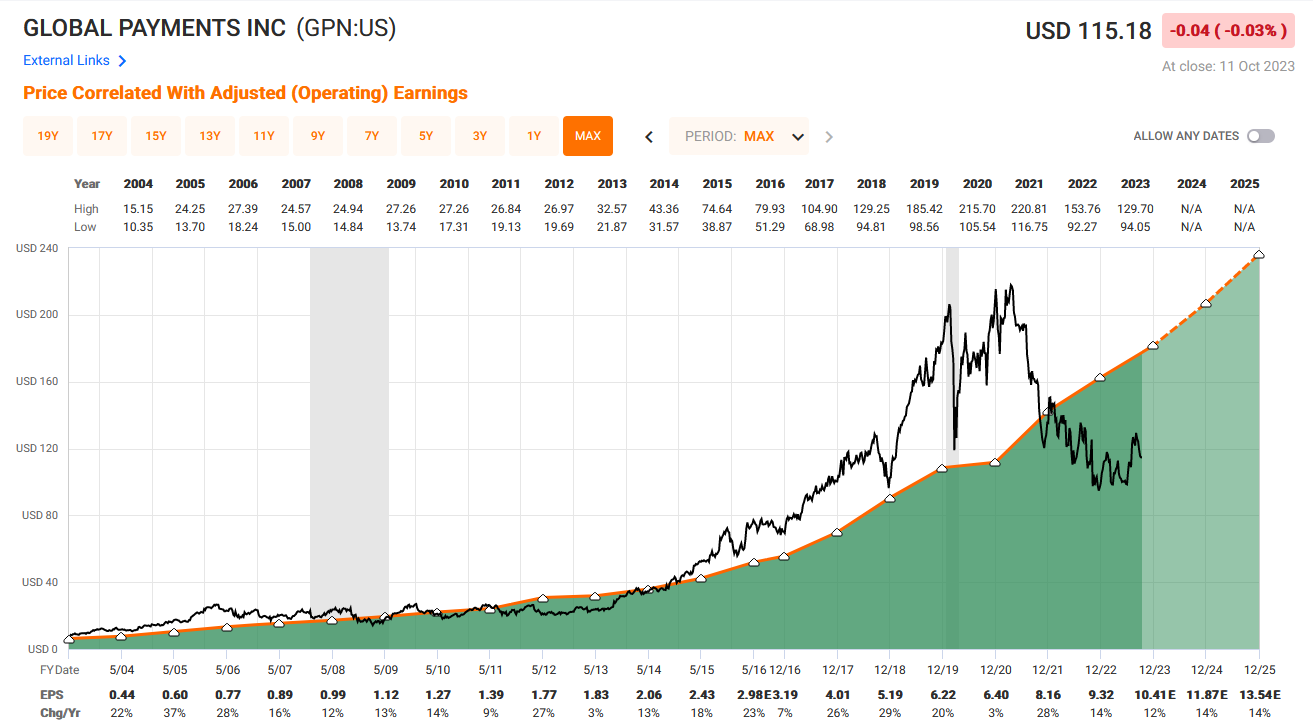

FAST Graphs Analysis

The FAST Graphs software is a powerful tool used to analyze the earnings of a company compared to the share price. The black line is share price and the orange line is earnings multiplied by 15.

Global Payment went through a period of overvaluation where the share price ran higher than the earnings warranted. Now the recent downturn has brought the company into fair value, and maybe even under value based on looking at the FAST Graphs.

Bull Thesis

Global Payment looks to be undervalued based on the earnings growth that it could experience in the future. The earnings growth rate is expected to be 14% annualized for the next few years. This would be a good return for the current valuation. The goal of the portfolio is to return 15% per year. The company is well positioned to keep growing based on its global presence and the move globally to transition to online payments only. GPN also has what is called the network effect. The more customers and businesses that join its network, the more valuable it becomes, making it increasingly difficult for new entrants to compete. GPN is also resilient towards market cycles and downturns. During economic downturns, people continue to make payments, making the payment industry relatively recession-resistant.

Bear Thesis

This market has intense competition for payment processors. Most small businesses already have their payment processor that they trust and don’t want to switch. Small businesses put a lot of faith in their payment processor won’t make a switch very readily. This benefits GPN keeping their current customers however it makes it difficult to gain new customers.

The credit cards have the pricing power and GPN is a price taker from the credit card companies. The interchange fees applied can affect the revenue and the profitability of GPN. The valuation currently is dependent on the growth rate of the company at a current valuation of 38 P/E. The growth rate of 14% isn’t enough of a growth rate to justify its high multiple valuation.

There are some risks to the growth rate. The payment processing industry has become saturated with competition and the room for growth isn’t as ripe as it has been in the past. The growth rate is also at risk from being a price taker from the credit card companies. Credit card companies could raise fees and increase costs for GPN.

GPN is also in an industry where technological changes happen rapidly, and GPN could be the odd one out on a new change. An example of potential risks is crypto currency block chain transactions, central bank digital currencies, or things like apple pay. These things could lead to a shifting away from Global Payment.

Rating

Basil Leaf Capital rates Global Payments as a BUY. Global Payment is a fair valuation for their current business. At fair value the company should continue the growth that they are seeing currently. They have the network effect working for them. Along with growth in the amount of customers using their service they also grow as their customers grow. The more business that the small business gets the more they are paying Global Payments. This company has proven its ability to be on the forefront of innovation so they should be able to adapt to new trends that hit the industry. As Warren Buffet said “Its better to buy a good company at a fair price than a fair company at a good price.” This is a good company at fair value with good returns opportunity.