Summary

JNJ is rated SELL. JNJ is a solid company that is one of the most important companies in America’s pharmaceutical industry. JNJ just doesn’t have enough upside to meet our return on investment goals. Our goal is to achieve 15% return on investment and JNJ at best offers an approximately 8% return.

Understanding JNJ as a Business

Johnson & Johnson (J&J) is a diversified healthcare company known for its extensive range of consumer health, pharmaceutical, and medical devices products. The company’s revenue streams stem from three primary segments: pharmaceuticals, medical devices, and consumer health.

In pharmaceuticals, J&J develops and markets a wide array of prescription drugs across various therapeutic areas. Some notable patented products include Remicade (for autoimmune diseases), Stelara (for autoimmune and inflammatory disorders), and Darzalex (for multiple myeloma). The pharmaceutical segment focuses on innovation, continuously introducing new medicines while leveraging its existing portfolio. The pharmaceutical segment is a R&D heavy industry that is a large risk large reward. When drugs are under patent they can be largely profitable and cost a lot of money to make back all of the R&D investment they’ve poured into the drug along with funding R&D on other drugs. Patents last for 20 years however drugs are usually patented years before they are ready to go to market. Stelara is, from personal experience, a drug that works well for autoimmune disease and it costs an arm and a leg. Since autoimmune diseases aren’t curable yet the treatments are the continuously profitable segment of drugs.

The medical devices segment encompasses a broad range of products used in surgical procedures, orthopedics, vision care, and interventional solutions. J&J has patented devices like the Acuvue contact lenses and innovative surgical equipment and orthopedic implants, contributing significantly to this segment’s revenue. Orthopedic and Surgery products account for around 70% of the medical devices segment. Vision care and interventional solutions account for the other 30%. The interventional solutions products are the fastest growing part of the medical devices segment.

The consumer health segment includes well-known brands like Band-Aid, Tylenol, Neutrogena, and Listerine. These products span categories such as skincare, over-the-counter medicines, oral care, and women’s health. Many of these products maintain strong market positions and are protected by trademarks and patents, ensuring their uniqueness and value to consumers.

Additionally, J&J holds patents and intellectual property rights for various medical technologies and innovations, providing a competitive edge and supporting its ongoing research and development efforts across all segments. These patented products and technologies serve as key revenue drivers for the company, solidifying its position as a leading healthcare entity in the global market.

Valuation Metrics

The finviz stock screener is a great tool to see performance metrics that are important to assess a company’s valuation. JNJ is currently valued at $371 Billion by market cap. The current PE ratio is 29.47 and the forward PE ratio is 14.30. JNJ being valued at 15 PE would be a fair valuation for the company because the projected growth for the next 5 years is 5%. The earnings growth along with the dividends provides a solid return of approximately 8%. The current PE being 29 seems overvalued while the future PE would be reasonable meaning the share price shouldn’t increase while the earnings increase.

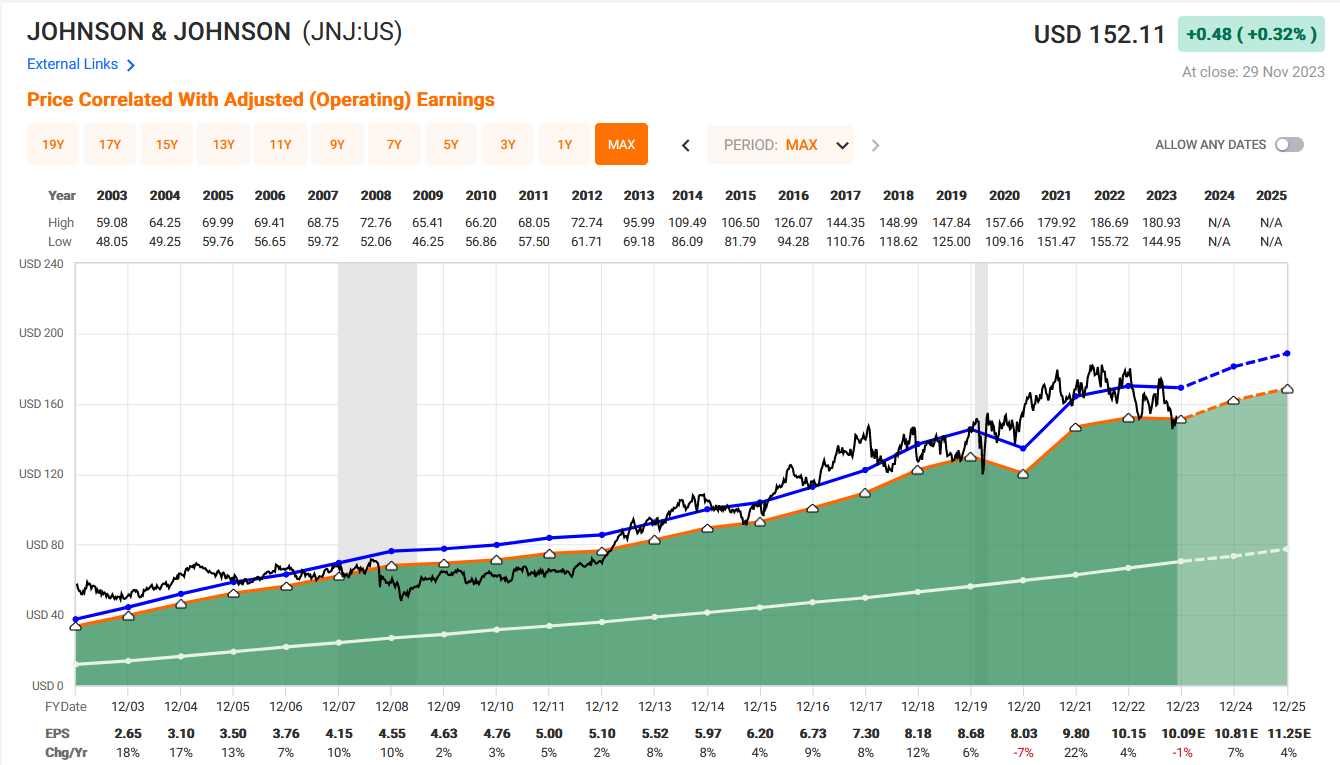

FAST Graphs Metrics

The FAST Graphs software is a powerful tool used to analyze the earnings of a company compared to the share price. The black line is share price and the orange line is earnings multiplied by 15.

Looking at FAST Graphs the share price currently looks fairly valued compared to the earnings. JNJ has historically traded at a premium and currently it is trading below its historic premium. JNJ also pays a dividend and that dividend being the white line has increased steadily over time. According to FAST Graphs analysis I would call JNJ fairly valued.

Bull Thesis

JNJ is a juggernaut in the medical and health space. They consistently produce high quality patented drugs to increase earnings growth and fund future R&D for the next drug. JNJ is also growing in the medical device space. The interventional solutions part of the medical device segment is growing at a remarkable clip and can drive that segment’s growth in the coming years. JNJ is expected to grow earnings at a rate of 5% for the next few years while offering a 3% dividend. This total return would be 8% with the upside of returning to the historic premium PE that JNJ has traded at in its history.

Bear Thesis

JNJ is a solid company that has proven itself to be a stalwart in the American economy. They have made themselves into one of the most important pharmaceutical companies. With all that being said the company is past its growth phase and isn’t offering a enough of a return on our investment to justify our investment. Our goal for our portfolio is to grow at 15% year over year and its not obvious how JNJ would help us achieve that return. JNJ would need something paradigm shifting for their company in order for them to grow at a greater rate to justify our investment. Another pathway for the return on investment to be there for us is if they increased the dividend by a large amount. This isn’t possible for them because they need to invest their free cash into R&D to keep their product pipeline healthy. JNJ could be a solid defensive portion of a portfolio that will consistently pay a dividend however it will not drive the return for the portfolio.

Rating

JNJ is rated SELL. JNJ is a solid company that has performed well for a long period of time however the upside opportunity is just not present for our investment. The bulls are correct to think this is a great American company however the bears are correct to acknowledge we won’t meet our investment goals with this company. If you hold JNJ in your portfolio you aren’t doing poorly you probably are just losing out on an opportunity for a higher return. JNJ has a place in defensive and income strategy to protect wealth however that is not the goal of our investments. If JNJ experiences a sharp down turn on some negative news it would be a good opportunity to buy a great company with the upside of the PE expanding. Until that happens JNJ is a SELL.