Summary

McDonald’s is rated SELL. McDonald’s is the premier fast food company with strong global brand recognition, healthy cash flow, and innovation with automation. With these strengths the earnings projections are expected to grow at 10% per year. This earnings growth combined with their dividend of 2% leads to an expected return of 12% per year. Not only does this not meet the investment goal of 15% return there is also a large downside risk to the earnings multiple contracting. McDonald’s is trading at a valuation far greater than its historic average could return to a lower earnings multiple.

Understanding McDonald’s as a Business

McDonald’s is the original fast-food business. The burger giant operates under a diversified revenue model comprising various streams. Primarily, its revenue stems from three key segments: company-operated restaurants, franchised restaurants, and rental income.

Franchised restaurants represent the largest portion of McDonald’s revenue. This revenue comes from franchise fees, rent, and royalties paid by franchisees. Franchisees pay initial fees and ongoing royalties for the right to operate under the McDonald’s brand, benefiting from its established business model, marketing, and operational support. Franchise fees are on average 4-5% of total franchise sales.

McDonald’s owns and operates several restaurants globally. Revenue from these outlets is generated through direct sales of food, beverages, and merchandise to customers. A majority of McDonalds are franchised and they prefer to franchise however they do own some of the stores. Generally McDonald’s restaurants operate at margins between 10% and 20%.

McDonald’s owns many of the properties where its restaurants operate. It generates revenue by leasing or renting these properties to franchisees, creating a steady income stream outside of direct sales. This property that they own isn’t usually the first thought however it is an important aspect to their book value.

In addition to these primary revenue streams, McDonald’s also earns income through various channels such as product licensing, strategic partnerships, and marketing tie-ups. The brand constantly innovates its menu offerings, introducing limited-time products or partnerships with other brands to attract customers and drive revenue growth.

The company’s global footprint and consistent brand recognition play a pivotal role in its revenue generation. By leveraging its well-established brand, McDonald’s continues to evolve its business model, adapting to changing consumer preferences and market trends to sustain and grow its revenue streams.

McDonalds initially carved out their success by inventing fast food and revolutionizing the restaurant business. Today there are a large amount of fast food restaurants today. From personal experience fast food is no longer that fast and the prices are comparable to traditional restaurants. As a consumer, paying high prices for low quality food while sitting in a long line in a drive through is not a competitive option for dining.

Valuation Metrics

The finviz stock screener is a great tool to see performance metrics that are important to assess a company’s valuation.

McDonald’s holds a commanding $207 billion market cap, and a price-to-earnings ratio (P/E) of 25 and a forward earnings ratio of 23. The company is anticipated to have a decent growth rate of 9.7% annually over the next 5 years. While the current P/E ratio indicates a substantial premium in relation to the projected growth, the promising growth forecast and McDonald’s established position in the market remain key considerations in evaluating its valuation.

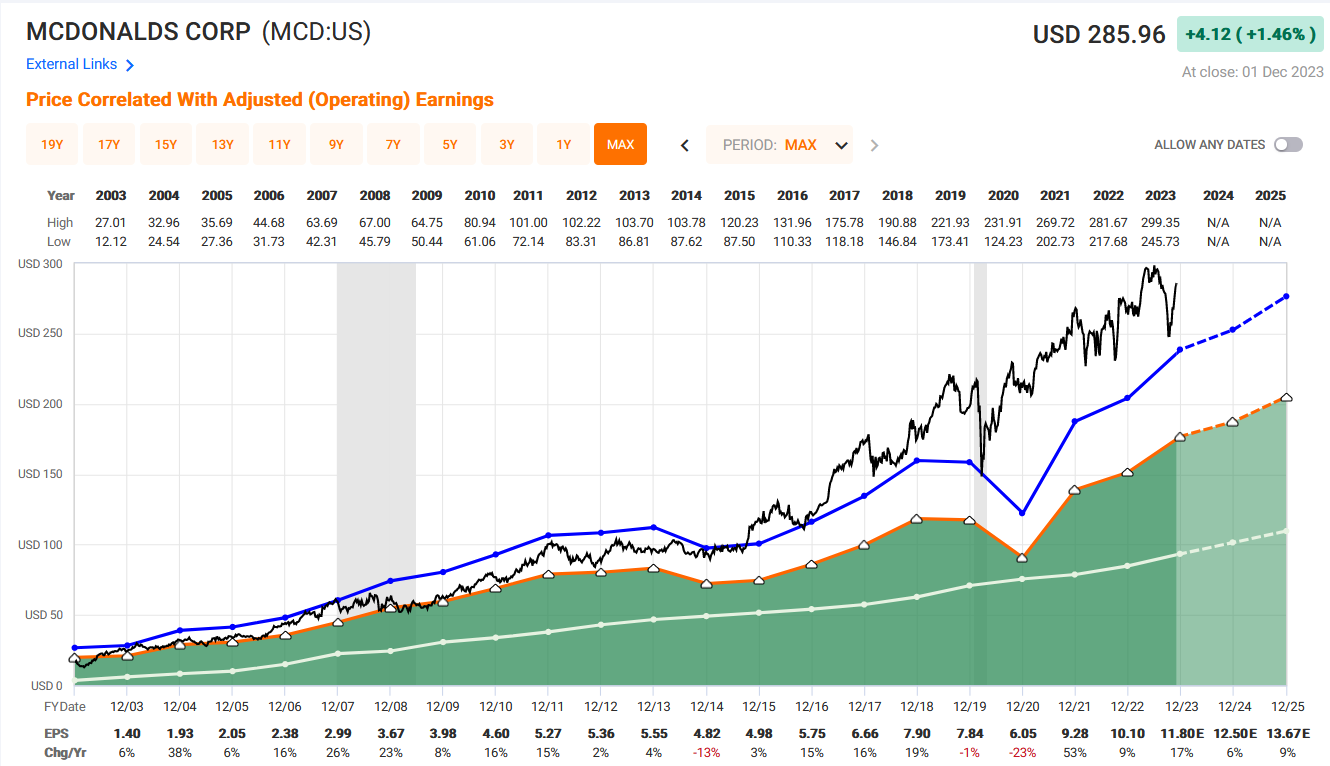

FAST Graphs Analysis

The FAST Graphs software is a powerful tool used to analyze the earnings of a company compared to the share price. The black line is share price and the orange line is earnings multiplied by 15.

McDonanld’s is trading at a large premium to their earnings. They are trading even greater than their historic Price to earnings ratio. The conclusion we can draw from the FAST Graphs analysis is that McDonald’s stock is overvalued compared to historical valuations. McDonald’s is not growing its earnings at its historical rates and is still valued at a higher multiple than its historical average.

Bull Thesis

McDonald’s is a stalwart in the fast-food industry as well as a global brand presence. McDonald’s boasts an expansive network of franchises across the world, offering consistent revenue streams. They are at the forefront of the automation of the restaurant industry. They were the first to introduce ordering kiosks and continue to improve the implementation of that technology. The implementation of automation will increase lower labor costs and increase margins. Additionally, the company’s robust cash flow supports its commitment to returning value to shareholders through dividends and buybacks, making it an attractive option for investors seeking stable returns and long-term growth potential.

Bear Thesis

While McDonalds did revolutionize the restaurant industry by inventing fast food, its growth days are behind it. It is no longer a high growth company, it is a stalwart slow grower. The current valuation is well above its historic earnings ratio and is trading at a premium as if it is a growth company. Not only is the valuation very expensive for the cash flow generated and expected earnings growth, the product is decreasing in quality. The fast food industry serves low quality food with subpar service. The only reason to eat fast food is when there is no other option available such as a time restriction or on a road trip. The combination of an expensive valuation and a low quality product makes this an unattractive investment. Our investment goal of 15% return on our investment is unlikely to be achieved by their earnings growth and dividend. The 10% earnings growth along with the 2% dividend offer a 12% return. This return is also assuming the earnings multiple remains constant. The earnings multiple is more likely to return to historic averages or even lower to a reasonable multiple of 15, than increase or remain constant.

Rating

McDonald’s is rated SELL. While McDonalds is a staple of the American economy, it does not offer the return on investment criteria for the portfolio. The goal is to achieve 15% return on investment and the earnings plus dividend are only projected to return 12%. Not only is the earnings projections not enough, there is also a downside risk to the earnings multiple contracting. Using FAST Graphs we can see that the current valuation is well above even its historic trading premium. The earnings multiple could revert lower to around a 15 earnings multiple. Not only is the valuation too expensive McDonalds is serving low quality products with poor service. Competition will take the opportunity to serve a better product and take some of McDonald’s market share. The bulls are right to value McDonalds brand strength, innovation in automation, and real estate portfolio, however the market is already overvaluing those factors in the premium earnings multiple.