Summary

Raytheon is a BUY. The base case of 14% return from the 11% earnings growth and 3% dividend offers a great level of safety. The bad news of the recall has provided a great opportunity to buy a powerhouse company at fair value instead of a premium. The return of the premium and the increased wars globally could drive even more return than 14%.

Understanding Raytheon as a Business

Raytheon is one of the largest aerospace and defense companies in the world. They specialize in a range of products and services in the defense,aerospace, and cyber security sectors. Raytheon operates in several key business segments:

Pratt & Whitney (P&W): As one of the world’s leading aircraft engine manufacturers, Pratt & Whitney designs, manufactures, and services aircraft engines used in a wide range of commercial and military applications. Pratt & Whitney engines power commercial aircraft, military fighters, helicopters, and more.

Collins Aerospace: Collins Aerospace specializes in the design and production of advanced aerospace and defense technologies. Their products and services include avionics systems, power systems, interior systems, mission systems, and more. They cater to both commercial and military customers, providing critical components and systems for various aircraft.

Raytheon Intelligence & Space (RIS): This segment focuses on developing cutting-edge technologies for defense, intelligence, and space exploration. RIS provides a wide array of services, including intelligence, surveillance, reconnaissance (ISR) solutions, cybersecurity, advanced imaging, and mission support for government and commercial customers.

Raytheon Missiles & Defense (RMD): RMD is known for its missile systems, precision weapons, and integrated defense solutions. Their products range from air and missile defense systems to advanced naval systems. The segment plays a vital role in bolstering national defense and supporting allied forces around the world.

Raytheon Technologies operates in a highly competitive global market. Its major competitors include Lockheed Martin, Boeing, Northrop Grumman, General Dynamics, and BAE Systems, among others. These companies also provide a wide range of products and services for the aerospace and defense sectors. Competition in this industry is driven by factors like technological innovation, cost-effectiveness, and performance reliability.

Valuation Metrics

The finviz stock screener is a great tool to see performance metrics that are important to assess a company’s valuation.

Raytheon currently trades at a value of $106 Billion by market cap. The current P/E ratio is 19 and the forward P/E is 13. The EPS is projected to grow by 11% for the next 5 years.The valuation for this company is reasonable based on its earnings and projected earnings. The earnings projections could be potentially low due to increased sales from the ongoing conflicts around the globe.

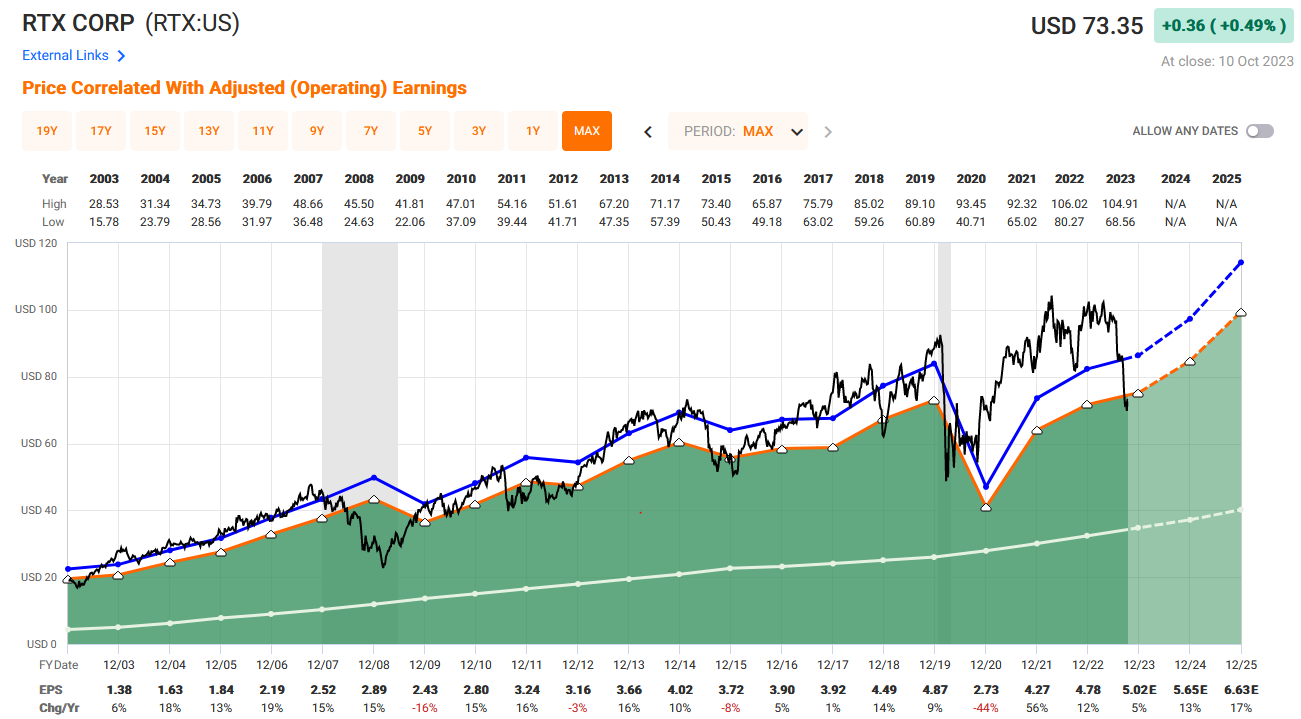

FAST Graphs Analysis

The FAST Graphs software is a powerful tool used to analyze the earnings of a company compared to the share price. The black line is share price and the orange line is earnings multiplied by 15. The blue line is the average PE ratio over the time frame plotted.

Looking at the graph we can see that recently the share price of Raytheon has come down to what would be considered fair value based on their earnings. Raytheon is expected to continue to grow based on what the analysts are projecting.

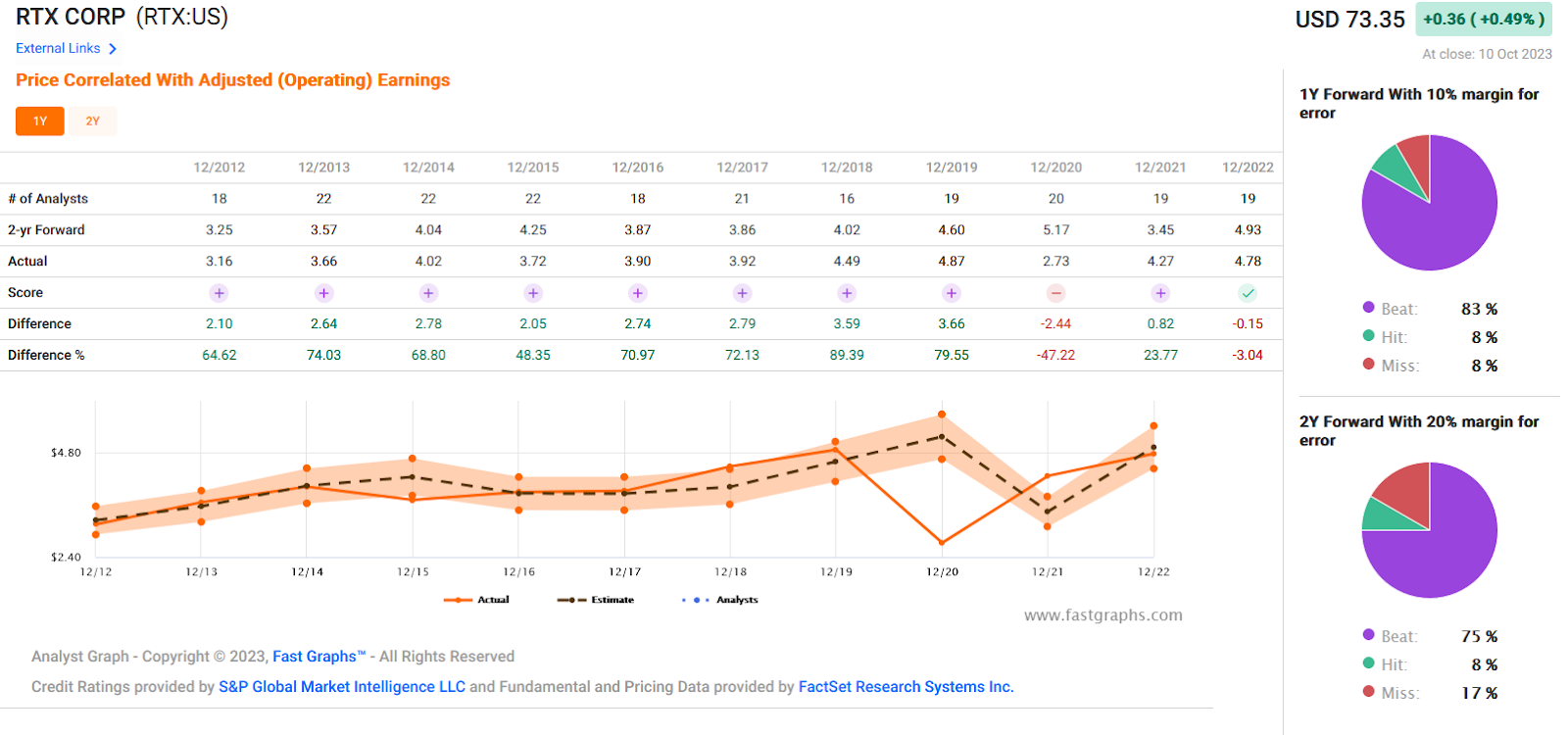

As we can see from the analyst scorecard the analysts are usually pretty good at predicting the earnings and even are too conservative on their earnings. The stability of their business as well as analysts track record mean that we can reasonably trust the analysts projections.

Bull Thesis

Raytheon is a defense contractor power house. With the volatile nature of the current geopolitical stage, Raytheon is well set up to profit from these conflicts. Raytheon has recently come into fair value and is projected to continue to grow at 11% annualized return. This earnings return combined with the dividend yield of 3%. The 11% gain plus the 3% yield provides us 14% return on investment. The earnings could potentially grow at an increased rate than 11% with the new conflicts globally and increased defense spending from the US gov. Historically Raytheon has traded at a premium valuation of a P/E between 17 and 20. If we see a reversion to the typical premium placed on the company we could see even more return than 14%.

Bear Thesis

The precipitous drop in share price came from a recall on an engine from one of their most famous and popular engines from Pratt and Whitney. This recall is going to cost the company billions of dollars in free cash flow. This recall could have a large impact on the earnings for this year. This could affect the relationship that Raytheon has with its customers and drive their customers to the competition in the future. This would put the future earnings into question.

Even if the recall turns out to not affect the company negatively the return on investment doesn’t offer enough upside to warrant investment in this portfolio. Our goal is to achieve 15% return on our investment,and the 14% return doesn’t meet our goal. 14% return being the base case for the investment without factoring in the downside risk from the engine recall.

Rating

Basil Leaf Capital rate Raytheon a BUY. This is a great opportunity to add a stalwart powerhouse company for fair value. This type of opportunity usually only comes off the back of a series of bad news such as the engine recall. With the recall you need to ask if this will change the long term prospects of the company? I think in 5 years Raytheon will still be a powerhouse defense contractor that is pulling in earnings due to global conflicts and increased defense spending. The base case of 14% earnings should still be valid with the potential upside from new wars globally and the historic premium placed on the company. Analysts have been able to predict Raytheon’s earnings with good accuracy and therefore it should be reasonable to believe in the base case. The bear case thinking the recall will change the long term performance of this company is overblown and we are seeing an over reaction and that is what is creating the opportunity to buy this company at this price. Opportunity arises when there is fear and uncertainty.